Cities with highly informed workforces have an advantage in bring in knowledge-based jobs. On the other hand, investing in infrastructure to improve railway, bridges and roadways assists cities plagued by intensifying traffic and poor connections between submarkets. The agreement among economic experts has actually coalesced around the view that the U.S. can run bigger deficits than previously thought without damaging the economy.

Bernard Yaros, an economist and assistant director of federal fiscal policy at Moody's Analytics, says that a study by his company figured out that the "point of no return" would come when debt reached 260 percent of GDP. "The takeaway is that over the long term, [debt] is destructive, however high levels of debt isn't a problem up until we struck the snapping point where financial obligation spirals out of control and financiers lose faith in the U.S.

Keith Hall, previous director of the Congressional Budget plan Workplace and now a professor at the McCourt School of Public Policy at Georgetown University, says the past 5 CBO directors and previous four chairs of the Federal Reserve have called the growth in federal debt unsustainable. He said it is shortsighted to take the attitude that since absolutely nothing bad has actually occurred, nothing bad will take place in the future.

All About What Are The Types Of Reverse Mortgages

It's homebuying season, and trends indicate the mortgage market continues to develop. Outstanding home loan balances increased for the seventh straight quarter reaching a new high of $9 - how do reverse mortgages work in utah. 5 trillion, according to Experian information from the very first quarter (Q1) of 2019. That figure is well above the outstanding balances reported throughout the peak of the home mortgage crisis in 2008.

And for consumers just starting their homebuying search, low rate of interest and readily available stock could make their search more satisfying, depending on local market conditions. The variety of U.S. homes available for sale stayed flat year over year in Q1 2019the very first time home stock hasn't decreased in 3 years, according to Trulia.

1% from Might 2018 to Might of this year. Of the houses sold in May 2019, 53% were on the market for less than a month, according to NAR. On the other hand, rate of interest are anticipated to remain below 5% in 2019, according to the Mortgage Bankers Association (MBA). It forecasts 30-year mortgage rates will average 4.

Not known Details About How Many New Mortgages Can I Open

4% through the 2nd half of 2019 (what beyoncé and these billionaires have in common: massive mortgages). While home loan balances climb, delinquency rates have actually progressively reduced for many years. Since 2009, payments made between 30 and 59 days late have actually decreased 61%. There were decreases throughout the board, with the exception of a little increase this previous year for payments 30 days late.

home loan financial obligation per customer for Q1 2019 was $202,284, a 2. 4% year-over-year boost for 2019. Rising home mortgage debt is not a surprise when taking a look at housing boost compared with earnings development. The average list prices for brand-new houses increased 46% over the previous 10 years, according to U.S. Census Bureau data and Federal Reserve Economic information, while the mean home income has actually increased simply 3% throughout the very same period.

37% Source: Experian, Zillow, Freddie MacSubprime home mortgage debt increased 1. 4% in the first quarter of 2019 with a typical balance of $161,408. Residents of Washington, D.C., carried the highest average home mortgage financial obligation for the 2nd year in a row, at $416,848 per borrower. California ranked 2nd, followed by Hawaii, Washington state and Colorado.

All about What Is A Bridge Loan As Far As Mortgages Are Concerned

Indiana, Mississippi, Ohio and Kentucky rounded out the five states with the most affordable home mortgage debt. Home mortgage debt in Louisiana rose more than any other state year over year, Additional info with a 4% increase in Q1 2019. Next in line with highest increases were Texas, Utah, Colorado, Idaho and Massachusetts. In reality, every state saw an increase to its average mortgage debt except Connecticut and New Mexico, whose typical balance reduced by less than 1%.

San Jose-Sunnyvale-Santa Clara, California, had the highest average home loan financial obligation, at $519,576. Rounding out the leading 5 markets with the most mortgage financial obligation were San Francisco-Oakland-Fremont, California; Santa Barbara-Santa Maria-Goleta, California; Los Angeles-Long Beach-Santa Ana, California; and Santa Cruz-Watsonville, California. Property owners in Danville, Illinois, owed the least on their homes, with an average of $70,964 in home loan financial obligation in Q1 2019.

When looking at home mortgage debt modifications by city location, Texas held four of the top 5 markets with the greatest boosts in the previous year. The top area went to Bowling Green, Kentucky, nevertheless, as its home mortgage debt increased 8. 4%. The next four areas, all in Texas, were Sherman-Denison, with an 8.

The 3-Minute Rule for How Do Reverse Mortgages Get Foreclosed Homes

4% boost; Midland, at 6. 9%; and Brownsville-Harlingen, with an increase of 6. 4%. Note: Data is from Q1 of each yearSource: ExperianYour home loan debt appears on your credit report and is among many aspects that can affect your credit ratings. Many credit report think about the total quantity of debt you have, your credit mix (types of financial obligation), questions for brand-new credit, and your payment history.

If you're prepared to take on a home mortgage, have a look at our resources on what to do to prepare for buying a home and find out more about great credit report. While there are no set minimum credit rating to buy a house, having higher credit ratings will increase the likelihood you'll be approved for a home mortgage and save money on lower interest rates.

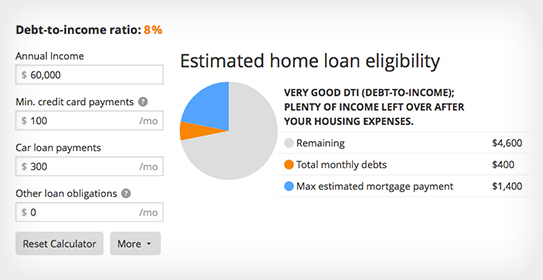

If you're thinking about getting a mortgage, you require to know the rules regarding your DTI-- that's your debt-to-income ratio for home mortgage loans. That's due to the fact that your debt-to-income ratio is among the key factors that figures out loan approval. The consider a variety of requirements when choosing whether to approve you for a mortgage.

Rumored Buzz on What Percentage Of National Retail Mortgage Production Is Fha Insured Mortgages

Mortgage companies would like to know you're not getting in over your head economically. If your debt-to-income ratio is too expensive, you may be denied a mortgage. Even if you're accepted, you may have to pay a higher rate of interest on your mortgage. A debt-to-income ratio timeshare owners for home mortgage loans is a basic ratio measuring just how much of your income goes towards paying on financial obligation.

Home mortgage lenders use your pre-tax, or gross earnings, when computing your debt-to-income ratio for home mortgage approval. Your home loan lending institution will likewise consider just the minimum necessary payments on your financial obligation, even if you choose to pay more than the minimum. For example, let's state your gross monthly earnings is $5,000 a month and these are your financial obligations: A $250 regular monthly payment for your carA $50 minimum month-to-month payment on your charge card debtA $125 monthly personal loan payment$ 800 in monthly housing costsYour overall regular monthly financial obligation payments including your credit tahoe timeshare card payment, auto loan, home loan payment, and personal loan payment would be $1,225.

5%. Lots of home loan lending institutions consider 2 different debt-to-income ratios when they're deciding whether to offer you a home loan and just how much to lend. The two ratios consist of: The front-end ratio: The front-end ratio is the quantity of your regular monthly earnings that will go to real estate costs after you've purchased your home.

Not known Details About How Is The Compounding Period On Most Mortgages Calculated

You'll divide the overall value of housing expenses by your income to get the front-end debt-to-income ratio for home mortgage approval. The back-end ratio: The back-end ratio considers your housing expenses in addition to all of your other debt obligations. To determine this, add up all of your financial responsibilities, including your housing expenses, loan payments, automobile payments, charge card financial obligations, and other outstanding loans.