Rate of interest as well as costs will certainly remain to build up on the financial obligation while you try to exercise any one of the above alternatives. Additionally, successors have noted that servicers commonly won't bargain and don't connect during the exercise procedure, and residences wind up being foreclosed in many cases. If you take out a reverse home mortgage, you can leave your house to your heirs when you pass away-- yet you'll leave much less of a property to them. Your heirs will certainly additionally need to deal with paying off https://finnjfcl.bloggersdelight.dk/2022/04/22/what-are-current-home-mortgage-prices/ the reverse home mortgage, or else, the lending institution will likely foreclose. With fixed-income assets paying next to nothing nowadays, reverse mortgages may be a beneficial means to fund day-to-day living expenses.

- The high expenses of reverse home mortgages are ineffective for the majority of people.

- It's smarter than a great deal of things people do while trying to get more income out of their nest egg.

- If you work out the alternative early after that you are paying a truck load in rate of interest along the road.

- A reverse home loan enables home owners to money in some of the equity in their residence as well as use the money whatsoever they want.

- The provider pays you a reduced (' marked down') amount for the share you sell.

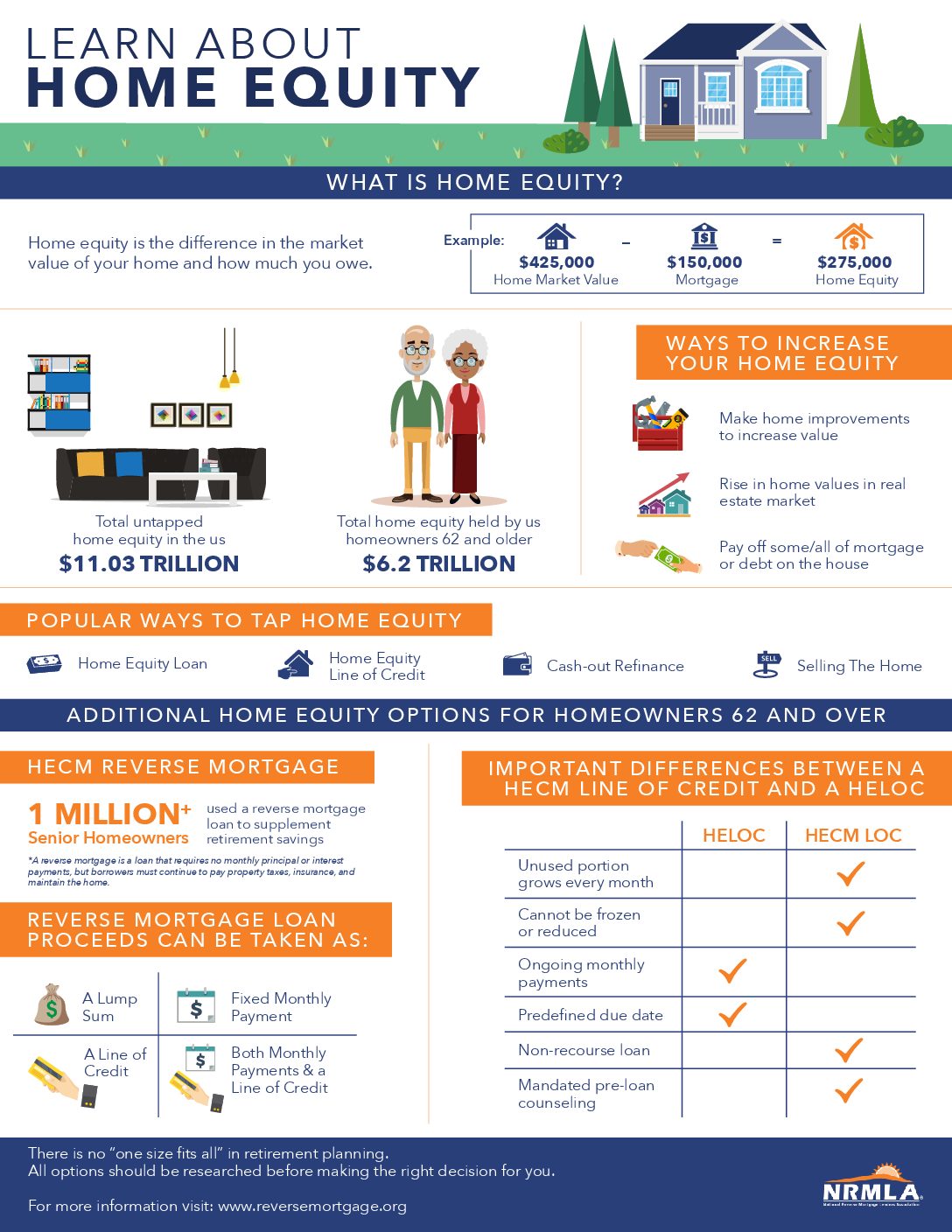

The minimum certifying age for a reverse home mortgage is 62. If you are within 6 months from your next birthday celebration, I will automatically calculate you a year older. You'll additionally obtain billed approximately $30 to $35 each month as a service fee. The total is billed based upon your life span. If you are expected to live another one decade you'll be charged one more $3,600 to $4,200. That figure will certainly be deducted from the quantity you receive.

Is A Reverse Mortgage Worth Truth Price?

In a reverse home mortgage, the loan provider pays to the house owner as opposed to the home owner paying to the lender. Because the house owner receives settlements from the loan provider, the property owner's equity in the home lowers gradually as the funding balance gets bigger. The reverse home loan may leave you with far much less money to live out your life when it does come time to offer up. Often referred to as "lifetime financings", reverse home mortgages use the equity in your home as safety and security for a car loan. As opposed to normal car loans, reverse home loan rate of interest is included in the car loan principal and also the whole lot is settled when you sell your house or die.

Share This Story: Is A Reverse Home Mortgage Worth The True Cost?

Get independent financial or lawful suggestions prior to you go ahead. Estate intending lawyer, or a customer protection attorney prior to securing this kind of lending. Yet the standards do not protect against the servicer from pursuing a foreclosure during this time. In fact, HUD's policies need servicers to launch repossession within 6 months of a default.

If you're not a huge fan of lendings, as well as you're not a huge fan of annuities, you could not be a large fan of reverse mortgages, which integrates both principles. You could be able to borrow more money with an exclusive reverse home loan. Yet the even more Additional resources you obtain, the higher the fees you'll pay. A HECM counselor or a loan provider can aid you contrast these kinds of fundings side-by-side, to see what you'll get-- and what it costs. With a reverse home mortgage, the home stays in your name. As well as because the residential or commercial property remains in your name, you are accountable for paying all property taxes.

Among the misconceptions bordering reverse home mortgage troubles for beneficiaries is that they will certainly be landed with a big bill when you die. As soon as your home is sold, the loan is website settled with the earnings and your successors obtain the remaining amount of equity. Your estate has 180 days after the notice of fatality to settle the lending. If you decide to move from your principal home, you will certainly have 180 days to resolve the loan with HomeEquity Financial institution.

Our editorial team does not receive straight settlement from our advertisers. Nonetheless, in the age of Covid-19, Americans may choose that large groups of older individuals cohabiting in one area could not be an excellent idea besides, McClanahan claims. This might indicate that more people will attempt to age in place. Property owners who are age 62 or older can transform part of the equity in their home into cash money rather than having to market. Discover funding offers with prices as well as terms that fit your needs.